What are the top financial tips for millennials?

Here’s my top 5.

#1 Save at least 20% towards future you.

I know saving 20% is a lot of your hard-earned cash, but the more you save now, the more options you have later. A host of things ranging from extra student loan payments to building up a cash, emergency fund can count towards this 20% number. The main thing is that you aren’t spending the money NOW. There are two reasons for this:

- The more you spend, the more you need to save. Most people don’t dramatically change their spending in retirement. If you want to support a $200K / year lifestyle, you need to save about $1.2M more than if you have a $150K /year lifestyle. Want to run the numbers yourself? Here’s another resource to see if you’re on track.

- Saving 20% gives you optionality. Most models suggest that you need to save at least 10% of your pre-tax income each year starting in your early 20s to be able to support yourself in retirement. If you took time off for grad school OR if you have multiple goals that you’re saving for like a down payment on a home or a college fund, saving 20% gives you enough for retirement plus some other goals. If you’re starting to save for retirement in your 30s, you may need to bump this up to saving 25% or more of your pre-tax salary. The early you start saving, the more choices you have.

#2 Don’t spend more than 30% of your pre-tax income on housing.

I get it. If you live in San Francisco or New York that might feel like a pipe dream. However, the more spend on housing, the less you have left over to spend on food, retirement, and living your life. Imagine you’re earning $120K in San Francisco. That’s a pretty good salary, no? When you take out federal and state taxes, you’re left with $83,067. Divided by 12 that equals $6,922 / month. If you’re spending $3.5K / month on housing, that leaves only $3,422 for everything else! While you can try to cut back your lattes and avocado toast that’s chump change next to spending less on rent. If you can live with roommates and spend $2.5K versus $3.5K that’s $1,000 in savings EVERY month. The same goes when you’re buying a house. The bank will generally approve you for a mortgage up to 28% of your pre-tax income. If you can keep your housing to 20% or lower, you’ll have much more money left over for childcare, student loans, retirement, vacationing on the Italian Riviera, whatever you want.

This is the one of my financial tips for millennials that is the hardest for people to stomach. However, if you can have the discipline to buy or rent less, you won’t regret it.

#3 Have an emergency fund

Everyone should have 4-12 months of your monthly expenses in an emergency fund. This money is there for you if you lose your job, have unexpected medical bills, need to take time out of the work force to care for a loved one, etc. This cash lets you sleep at night and also keeps you from EVER going into credit card debt.

How do you decide how much to have? The below table is a good resource.

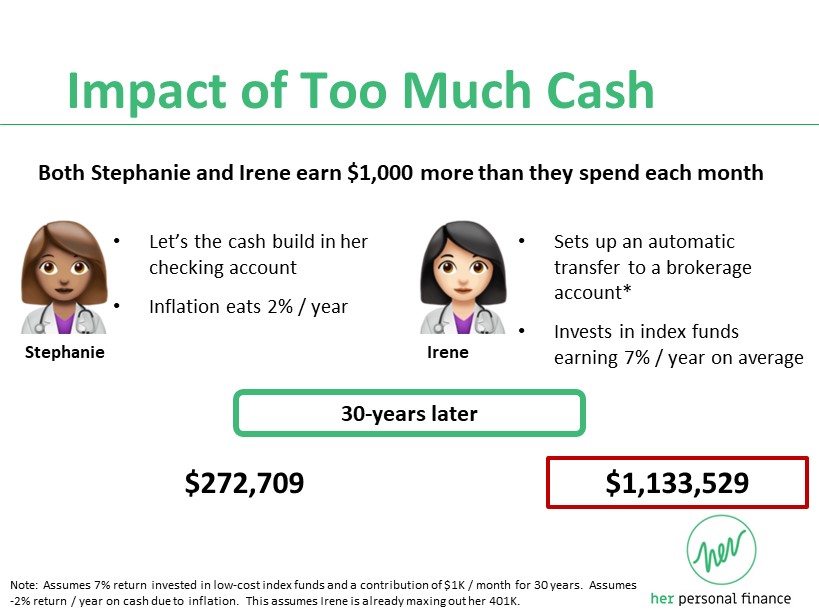

#4 Don’t keep too much cash

Outside of your emergency fund and money you’re allocating to a big goal in the next 2 years (like a house down payment), you don’t want to keep too much money in cash. Why? Two reasons. Inflation and performance returns. Cash is LOSING value every day. A McDonald’s Hamburger cost $0.62 in 1967 and costs $2.49 in 2021. Inflation has averaged 3.1% / year in the United States. At the same time that cash is losing money, you’re also not giving your money the opportunity to grow. While investing is always risking, the broader US stock market has averaged 10% / year. Adjusted for that 3% inflation, your money could still be growing at ~7% / year in the stock market. See the below example.

#5 Don’t try to optimize your retirement returns, focus on consistent savings.

It’s easy to listen to the market news and to get excited about Bitcoin or the latest meme stock. However, as the New York Times shared in this article about GameStop, “Timing a trade perfectly is nearly impossible even for the best stock pickers, so even those who made money missed out on far greater riches if they didn’t sell at the rally’s peak.”

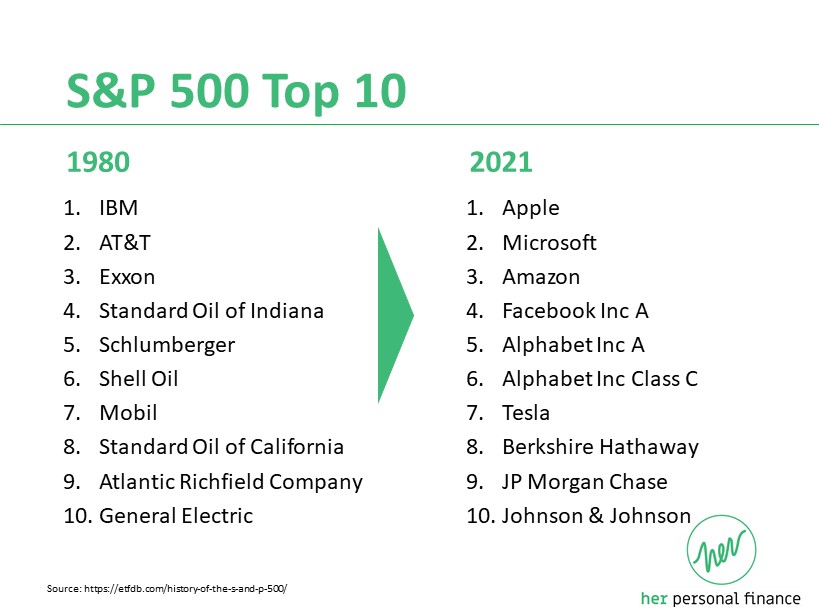

Instead of trying to pick “winning” stocks, I prefer to invest in a basket of stocks, my favorite example of which are called index funds. I don’t have to pick the next Apple or Tesla. I can invest in an index that tracks the biggest 500 companies in the United States. . As companies grow and shrink, this list changes over time. In fact, see below for how this list has changed from 1980 to 2021.

Not only is investing in index funds easier, but it’s also historically generated great returns. Remember the average stock market returns that I shared above? The largest 500 companies in the United States have consistently averaged 7% / year inflation-adjusted growth for the last 50 plus years. Yes, there are down years over that period of time and there is no guarantee the market will continue that trend. However, you can do VERY well if the market just keeps with that average, boring return.

One of my favorite hands-off way for people to invest for retirement is through Target Date Funds. These funds automatically shift from more stock index funds to more bond index funds over time making investing as hands off as possible.

Thanks for reading this far. These tips have been gleaned after reviewing the finances of hundreds of women through my 10-week bootcamp. In this class, I help women figure out how much to save for retirement, how to navigate Roth vs. Traditional 401K taxes, how to decipher between an ETF and a stock, and more. I would love for you to keep in touch!