Is a house a good investment?

You may have heard that “renting is throwing money away.” Your Uncle Ted may also have told you that “his house was the best investment he made.” Yet, in today’s market, much of that advice does not hold. Want to know why not to buy a house and why we choose to rent?

I’m a late 30s married woman with a child in the Austin area. I’m also a Harvard MBA and financial educator who has taught hundreds of students about investing, making a plan for student loans, etc.

I’ve run the numbers and renting makes more financial sense for me and family right now.

Here’s the math.

I’m using as an example a property that we rented in east Austin and moved out of in June 2023. We rented this house for $3,100 / month, and Trulia, Zillow, Realtor and others estimate the property at $707K – $737K in July 2023. In the below article, I will start with the five high-level reasons we have chosen not to buy a house or this house in particular. I will then share a more detailed pro forma breakdown.

Buying a house would more than double our cost of housing TODAY.

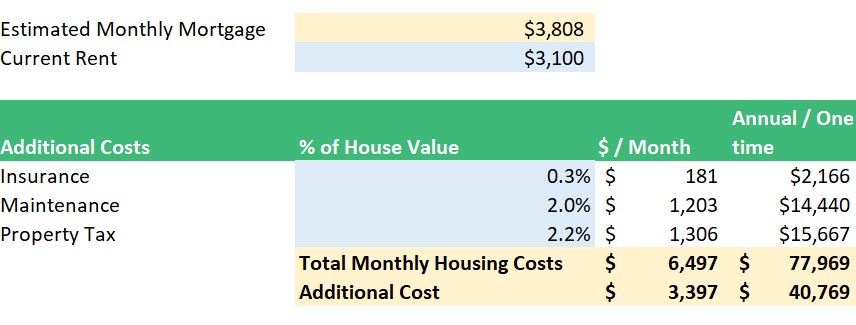

Our rent was $3,100 / month.

At July 2023 interest average interest rates for a 30-year mortgage in Texas average 6.91%. That means, assuming our house was purchased for $722K, at 20% down, our mortgage payment would be $3,808 / month. However, on top of the mortgage payment, we would also owe property taxes, home insurance, and would have to maintain the property. Texas and Austin specifically has high property taxes so our all-in housing payment would be ~$6,497 / month (see detailed breakdown below).

That is $3,397 / month more than our rent of $3,100 / month.

Of those expenses, many like property taxes and home insurance are not equity building. I also estimated some monthly maintenance costs. Many experts estimate maintenance will cost you 1-4% of the value of the home. Older homes tend be more maintenance. Since our house was built in the ’90s, I assumed 2% maintenance costs. Many individuals leave out maintenance, property taxes, and insurance when choosing to own, but it’s a key reason why not to buy house.

Renting helps keep housing costs a low percentage of income

In general, housing should be less than 28% of your gross income. Many banks will use this metric to determine what you can afford. While most calculations will exclude maintenance costs from these numbers, to comfortably afford a $722K home, that still means an income of $226,000 or higher.

In contrast, the rent number of $3,100 / month only requires an income of $133,000.

I’m an entrepreneur building a financial education business to help high-earning woman take charge of their financial future (check out my classes at herpersonalfinance.com). While I’m in the first five years of growing a business, I value the flexibility to take a low salary and invest back more into the business. Keeping housing expenses low is a big reason why not to buy a house.

Renting allows us to invest more

By keeping our housing costs low, we are able to invest more. According to the Case-Shiller index, Housing prices appreciated at an average rate of 5.24% from 2001 to June 2023 in the United States. During that same period, the S&P 500 grew 7.3% or 2.1% more than housing appreciation. Looking at a longer time horizon, real estate has averaged just over 4% per year growth while the stock market has more consistently averaged 9% before inflation.

By renting, we get to invest money that would otherwise go to a down payment. Over 30 years, investing $140K, a 20% down payment on a $700K house, would become $1.065M at 7.3%, average stock market growth. At a 5.2% growth rate, that same $140K would grow to only $640K.

On top of this difference, paying $3.1K instead of $6K+ in monthly housing costs, allows us to invest more in our 401K, IRAs, and brokerage accounts on a monthly basis.

Renting gives us flexibility to move

My husband and I are still new to Austin. We are still adjusting to a new city as a couple and we added a small child last year. While we figure out the right schools and part of town for us, renting gives us the flexibility to move.

Plus, this summer we chose to end our lease and spend 8 weeks in Boulder, beating the Texas heat. While we could choose this option while owning a home, we would either have to leave our home empty or put in the work to find a trusted short-term renter. Flexibility is a key reason why not to own a house.

We aren’t responsible for home maintenance

Any homeowner knows that things break. As a renter, when we discovered the air conditioning system was backing up and causing water to pool under the wood floors, we got to call the property management company and let them handle the mess. When you own, the money AND time required to fix a property are on you.

We mentioned above most estimates place house maintenance at 1-3% of the cost of the home. Older homes are generally more expensive to maintain since they will require new appliances, HVAC, water heaters, etc. sooner than new construction. If you have a pool or will need to pay some to maintain the yard or shovel snow, your home maintenance will be higher.

Rent vs Buy Calculation

I have now reviewed the high-level reasons we choose to rent. Here’s how the math breaks down.

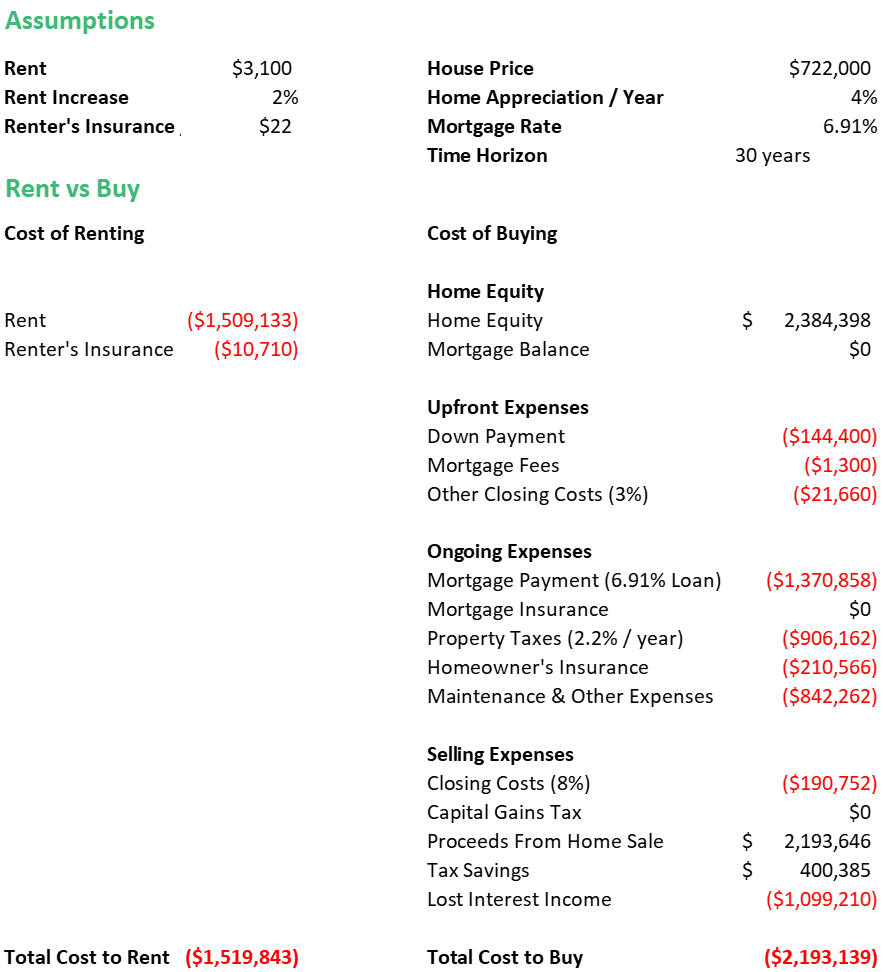

In the below model, at $3,100 / month in rent it is always mathematically better to rent versus own a house of $722K.

The math on renting is simple. It’s the cost of rent with an annual increase (here we use 3%) plus renter’s insurance. Buying is more complicated since you have to take into account the down payment, closing costs to buy, on-going costs including the mortgage payments, property taxes, and payments, and then closing costs again when you go to sell. Red numbers in parentheses indicate costs. Black numbers indicate an asset or incoming cash flow.

Over 30-years, using the below assumptions, renting would cost us ~$1.5M while owning would cost $2.2M. That’s over $700K more! And you wonder why not to buy a home…

30-Year Rent vs Buy Comparison

Assumptions and Sensitivity Analysis

This math is heavily dependent on how well our down payment would do if invested in the market instead of in a house. In the below numbers, we use 7% which is consistent with average stock market returns. However, if returns for the next 30 years are closer to 5% and real estate performs better than 4%, buying would become more advantageous.

Some individuals are predicting housing prices in Austin will fall because of the huge appreciation the past five years and an over saturation of Airbnbs If that happens, renting may be an even better choice until prices stabilize.

In this model, the home insurance costs, estimated tax savings, maintenance costs, and proceeds from home sale are taken from SmartAsset’s Rent versus Buy tool. At current interest rates, many individuals will experience considerable tax savings from buying a house since you can deduct the mortgage interest and up to $10,000 in State and Local Income Taxes (SALT).

Pros to Buying

While we have focused on the reasons to NOT buy, there lots of reasons to own a home.

Stability / Continuity

When you rent, you do not have control over the property and you may be forced to move. Our landlord decided to take the property back over to use as a home office. We had already decided to move, but renting means you may not have a choice.

You also cannot make changes to your home or have the pets or home situation you desire.

Taxes

In the above model, you may note that buying a house would save us money on taxes. The standard deduction for a married couple filing jointly is $27,700. However, the mortgage interest on this loan would be ~$39,700 in year 1. That means owning a home would allow us to deduct at least $12,000 more in taxes each year. At a 25% marginal tax rate, that is savings of $3,000 / year. Since you can also deduct up to $10,000 in property taxes and state income tax, in states like Texas where there is no state income tax, the tax savings of owning would be closer to $5,500 / year on a $722,000 home.

At current interest rates, the tax savings wouldn’t be enough to overwhelm the other costs of home ownership, but they’re worth noting.

Conclusion

Buying a house is both a financial and emotional decision. Long-term, I plan to own a home as a way to plant roots and get to know our community. However, in the short-term, we are saving considerable money by renting and are able to build wealth through the stock market at a faster rate than through home equity.

I hope that this helped you understand reasons why not to buy a house. I would love know what you think below.

About Me

I’m a former non-profit consultant and b corp employee passionate about trying to make the world a better place. More broadly, I am passionate about financial education. After I received my MBA from one of America’s top business schools, I realized that even the most educated of us have little formal education about our personal finances. In 2020, I launched a series of online courses to make financial education cheaper and more accessible. My goal is to help more high-earning women take charge of their financial future. I would love for you to sign up for my email list or join me on instagram (@her.personal.finance) for more financial education.

Uncover your money story and establish your financial baseline with this free resource that will help you chart your current money path and help you discover where your money currently flows.