If you have a 401K from work, you may have heard of Target Date Funds (TDFs). Many retirement plans default you to this option. Why? TDFs are one of the few “one and done” ways to invest. Instead of trying to pick individual stocks or bonds, TDFs allow you to invest across bonds, stocks, international and domestic options with a single investment which shifts over time to match your age. Once you have decided you want to invest in a Target Date Fund the next question is which one to choose. This article will explain Target Date Funds and will compare the options from Schwab, Fidelity, and Vanguard.

What are Target Date Funds?

TDFs change your investment allocation over time based on your target retirement age. They get less risky as you get closer to retirement and are designed to allow you to “set it or forget it.” As a result, >90% of retirement plans offer target date funds.

Many retirement funds choose TDFs as the option. As of the Pension Protection Act of 2006, TDFs are one of the few investments which meet Congress’s standards for an appropriate investment vehicle for most workers. While TDFs are more common in your 401K, you can also invest in TDFs through you IRA or your brokerage account.

Target Date Funds vs. Robo-Advisors

Target Date Funds were the precursor to Robo-Advisors. Just like a Target Date Fund, Robo-advisors like Betterment or Wealthfront rebalance your investments over time. However, Target Date Funds are focused on retirement. On the flip side, a Robo-advisor can adjust your investment mix to better align with the shorter-time horizon of buying a house or paying for a wedding in five years.

If you are focused on the investment options in your 401K, you likely WILL have access to a Target Date Fund but not to a Robo-Advisor.

How do you know something is a TDF?

Target Date Funds generally have a year in the name like Vanguard Target Retirement 2050 or Fidelity Freedom 2025 Fund. Funds with “Life Cycle” or “Life Stage” in the name may be how your retirement plan provides a similar offering.

Most brokerage firms including Schwab, Fidelity, Vanguard provide their own version of a TDF. While all TDFs have a similar philosophy, this article will dig into how these options vary.

What are the types of TDFs?

Some Target Date Funds are passively traded. They largely invest in ETFs or index funds. Others are actively traded and invest in mutual funds where someone picks stocks instead of tracking an index. This analysis will focus on the INDEX target date funds. One quick way to tell if something is an active TDF versus passive is the expense ratio (you can find this on any fund prospective). Expense ratios are the fees you pay for someone to manage this investment. Fees less than 0.2% indicate something is a passive fund. Fees higher than 0.2% indicate you are paying for an investment manager to actively pick stocks for you. A lot of data suggests passive funds outperform active funds since it is very hard to consistently beating the market.

How do Target Date Funds work?

Investment managers create a target portfolio based on your age and how close you are to the standard retirement age of 65. The funds shift from riskier and hopefully higher return when you are younger to more conservative and lower return as you get older. The idea underlying this philosophy is that when you are younger you have more time before you need to access your retirement funds. If the market falls when you are 30, you have 35 years to earn those dollars back. If you are 65 and ready to access your retirement funds, you may not be able to handle that market dip as easily.

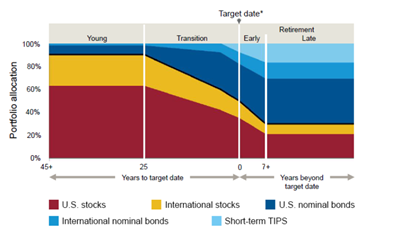

Below is an example of how Vanguard, the market leader in Target Date funds, invests over time. The below chart is what is called the TDF’s glide path. Do you see the shift from mainly U.S. and international stocks when you are younger and further from the target retirement date?

Someone 25 years away from retirement would have 95% of their money in domestic or international stocks. Someone 7 years away from retirement would have only 25% of their money in stocks and 75% of their portfolio in U.S. bonds, international bonds or Short-Term TIPS. (TIPS stands for treasury-inflation protected securities. These are bonds that move with inflation so you are protected even if the dollar is worth less).

Caveat: A common mistake that investors make is investing in more than one Target Date Fund. Target Date Funds are already diversified. You do not need to invest in more than one to have a diversified portfolio.

How does a Schwab Target Date Fund compare to Vanguard or Fidelity?

Vanguard and Fidelity are two of the biggest retirement plan operators. As a result, you may be the most familiar with their options. However, in 2016, Charles Schwab added a new portfolio of low-cost Target Date Funds. How do these options compare?

First, ALL Target date funds across all three companies invest in ETFs, or baskets of stocks, instead of individual stocks or bonds. Schwab US Large Cap ETF (SCHX) is the largest holding in most Schwab Target Date Index funds. Owning this means you own part of all the publicly traded companies in the U.S. As a result, you do not have to guess if Apple will perform better than Tesla over the next 30 years. You own them all! Schwab, Fidelity, and Vanguard have very similar strategies when approaching their Target Date Funds. However, they differ in how what they charge and how they choose to shift their assets over time.

Summary: Schwab vs Vanguard vs Fidelity

All three companies offer low-cost, diversified ways to invest for retirement. Schwab charges the lowest fees, but Vanguard has the strongest 10-year performance of the three. Their underlying investment strategies are very similar, but Schwab is slightly more conservative and Fidelity is more aggressive. You cannot go wrong with any of these options. The decision of which to choose may be simple. In your 401K, your company may only provide one of these options.

Cost: Schwab, Fidelity, and Vanguard all charge well below the industry average for their Target Date Funds. Schwab is the cheapest charging you 0.08% of your total assets, but Fidelity and Vanguard are also very low cost at 0.12% and 0.15% respectively. All of these fees are low. The average fee for Target Date Funds is 0.75%, and many managed accounts charge 1.5%. For someone with a portfolio of $100K investing $10K / year for the next 30 years, the difference in an 0.08% versus an 0.15% fee is only ~$30K. For that same individual, the difference in paying 1.5% versus 0.08% is over $523,000. Winner: Schwab by a hair.

*Note: if you buy one of these funds through your 401K, your employer may have negotiated a different expense ratio. Interestingly, the expense ratio may be higher within your 401K especially if you work at a smaller company.

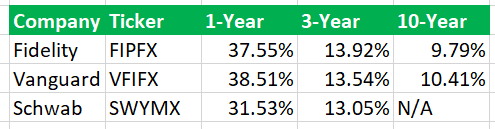

Performance: Vanguard was the first to come out with Target Date Funds so they have the longest performance history. Since the Vanguard Target Date funds were started in June 2006, they have achieved an average 8.47% return, and they had an incredible 43% one year return in 2020. Comparing the 3-year annualized performance of their Target Date Funds, Schwab, Vanguard and Fidelity all had strong returns of 12-14% / year. Since TDF investors are generally investing for retirement, focus on long-term performance over short term. See below for a detailed breakdown. Winner: Vanguard with 10.10% 10-year returns.

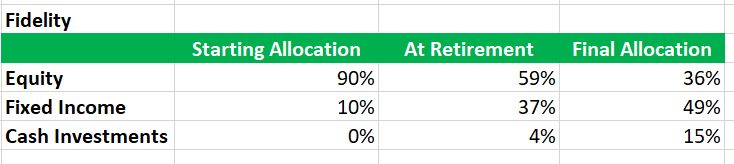

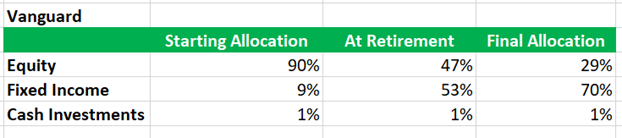

Risk: All three funds have similar investment allocations when you’re under 40. All three put 90% of your assets into stocks. However, as you get older, they diverge. Fidelity allocates 19% more of your money to stocks when you hit “target date”, generally 65. They have 36% in stocks when you’re 10+ years into retirement. This is 19% more in stock than Schwab allocates at “target date.” At the same time, perhaps to compensate for this heavy hand, Fidelity keeps more cash. Overall, Schwab is the most conservative, then Vanguard, followed by Fidelity. Winner: Depends on your individual risk tolerance. Fidelity is the highest risk option and Schwab is the lowest risk.

Note: if you have an old 401K that does not offer the Target Date Fund that you want, rolling over your old 401K to an IRA with that company can expand your investment options.

Glide Paths for Schwab, Fidelity, and Vanguard

The shift in assets over time is called a glide path. Below is a comparison of the glide paths for Schwab, Fidelity, and Vanguard.

Is it risky to put all your money in Target Date Funds?

Whenever you invest in the market there is risk. However, Target Date Funds create diversification and reduce your exposure to stocks over time. They keep you from having 100% or 50% of your retirement in a single or small group of stocks or bonds. In addition, they balance risk versus reward. The Vanguard Target Retirement 2025 Fund has had a 7.47% average annual return since it started in 2003.

Conclusion

Target Date Funds are a great “one and done” way to invest. They adjust your investments from more stocks to more bonds as you get closer to retirement age. Within Schwab, Fidelity, and Vanguard, the options are all similar. If you are looking for the longest-track record, strong performance, and low but not the lowest fees, Vanguard is the best option. However, Schwab and Fidelity have undercut Vanguard on fees, are generating strong performance, and are very viable options as well.

While which fund you choose matters, starting early and consistently investing will have a bigger role on your end retirement nest egg than the relatively minor differences between these options.

Uncover your money story and establish your financial baseline with this free resource that will help you chart your current money path and help you discover where your money currently flows.