Are Health Savings Accounts (HSAs) Worth it?

What is an HSA

A Health Savings Account (HSA) is a tax-advantaged savings account for medical expenses, available to those with high-deductible health plans (HDHPs). HDHPs are a type of health insurance plan that have higher deductibles and lower monthly costs compared to traditional health insurance plans. Most HDHPs are PPO (preferred provider organization) plans. This means you likely have access to the same doctors with a HDHP plan as you would with other insurance options.

For 2024, the IRS defines a HDHP as having a minimum deductible of $1,600 for individuals and $3,200 for families. HDHPs are often paired with HSAs allowing you to save money tax-free for medical expenses.

Since many individuals have a choice of a HDHP or a lower deductible alternative, here is more information on HSAs and how to decide if they are right for you.

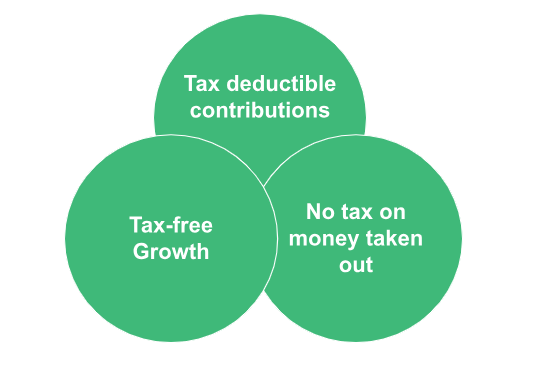

How it saves you on taxes

There are several ways an HSA account helps you save on taxes. Contributions made to an HSA are tax deductible and lower your taxable income for the year. Funds in an HSA grow tax free if you choose to invest the funds (note: this will NOT happen automatically). Additionally, withdrawals made from an HSA are tax free when used for qualified medical expenses like prescription contact lenses or doctor bills.

Making sense of health insurance

Deciding if you need an HSA can be difficult if you are not familiar with the terminology. Three important terms to know are: insurance premiums, deductible, coinsurance, and out-of-pocket maximum.

Insurance premium:

- An insurance premium is the amount you pay, typically on a monthly basis to maintain active coverage with your health insurance. This payment ensures that you stay covered even if you don’t use any medical services.

Deductible:

- A deductible is the amount you must pay on your own before your health insurance starts covering the costs. For example if your deductible is $2,000 and you have a $5,000 medical bill, you will first pay the $2,000 in medical expenses. At that point, your health insurance will start to contribute. If your plan has co-insurance (see below), you will pay a percentage of the bill over $2,000 until you have met your out-of-pocket maximum payment.

Coinsurance:

- Coinsurance is the percentage of costs you have to pay after you’ve reached your deductible. For example if your insurance plan has a 20% co-insurance payment, your insurance will cover 80% of the cost and you will pay for the additional 20%. The coinsurance lasts until you hit your out-of-pocket maximum. In the $5,000 example above, you would pay the first $2,000 towards your deductible. From there, you would pay 20% of the remaining $5,000 or an additional $1,000.

Out-of-pocket Maximum:

- Your out-of-pocket maximum is the maximum amount of money you can pay for covered medical expenses during a period of time, typically a year. Once you reach your out-of-pocket maximum, your insurance will pay 100% of the expenses moving forward for that year. If your out-of-pocket maximum is $5,000, you would not pay an additional funds e.g., no co insurance after you had paid $5,000. Your plan may have a different out of pocket maximum for in-network and out-of-network care.

HSA vs FSA

The difference between an HSA and an FSA is that an FSA typically has a “use it or lose it” rule within the plan year with limited roll over or grace period options. In contrast, HSA do not have a “use it or lose it” rule.

In other words, you do NOT have to spend the funds in your HSA each year. You can invest them! This can make an HSA part of your retirement strategy. If you save your medical bill receipts, you can take out HSA funds in the future as long as you can show you have had medical expenses in the past. For example, I could invest $3, 000 in an HSA and not spend the funds this year. If I had knee surgery and had $2,000 in out-of-pocket costs in 2024, I could save the receipts and take a $2,000 withdrawal from my HSA five years in the future. This can give you flexibility for when you touch your HSA dollars.

In contrast, an FSA is best for you if you want to set aside pre-tax dollars knowing you’ll have medical expenses that year and plan to use it within the year. A big perk of FSAs is they do not require having a HDHP. Some employers do not offer HDHP and since these plans, by definition, have a high deductible, FSAs can be a better option for individuals who want to pay less out of pocket for medical bills.

When to use an HSA

You should consider using an HSA plan if:

- You can afford the deductible in your high deductible plan. An HSA eligible plan could have a $3,000 deductible while the non-HSA eligible plan may have a $1,000 deductible. This means you may pay more out of pocket before your health insurance kicks in. Note that preventative care like a well-woman exam is generally provided at no cost to you even before you meet your deductible. The deductible for your plan will depend on where you buy your insurance. Plans with lower deductibles often have higher premiums.

- You don’t have a lot of expected healthcare costs. As stated above, HDHPs often have lower premiums but a higher deductible than a non-HDHP. If you know you will have $10,000 in bills this year because you are having a baby or going through IVF, a HDHP will lead to more out-of-pocket costs.

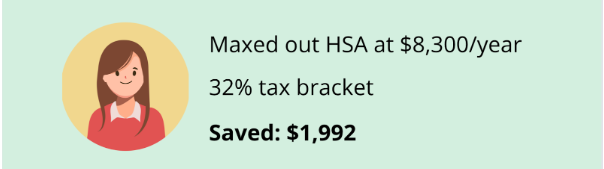

- You want to save more for retirement tax free. Money put into an HSA reduces your tax bill today. The more you earn, the more you will save on taxes. For example, if you’re a family and you earn $400,000 in combined income, you’re in the 32% tax bracket. Contributing the maximum $8,300 to an HSA in 2024, would save you $1,992 in taxes today. Plus, you can invest the $8,300 and any growth also comes out tax free. If that $8,300 grows at 7% / year for 30 years, your HSA balance could be over $63,000. You will not pay taxes on any of that money if you used it after 65 for any expense or before 65 for a qualified medical expense like a knee surgery.

When NOT to use an HSA

You might want to avoid using an HSA plan if:

- Your high deductible plan has a high deductible and / or out-of-pocket max and you know you will have a lot of healthcare costs. For example, if your high deductible healthcare plan has a $3,000 deductible and you have a mole removal and biopsy that costs $1,200, you would likely cover that entire cost.

- You’re not a super high earner and the tax impact isn’t that meaningful. The more you make, the more an HSA saves you on taxes. If you earn $60,000 as a single person and take the standard deduction, you may be in the 12% marginal tax bracket. Hitting the individual limit for an HSA of $4,150 would save you $498 in taxes. While $498 is a meaningful amount of money, the savings are greater for those in higher tax brackets.

- You don’t plan to stay in your job that long and don’t want the hassle of another account. We have all been there. Rolling over old 401Ks is annoying enough. HSAs are another account to contend with.

Which health plan is better PPO or HSA eligible HDHP?

This is a tough question that depends on your plan benefits.

Here’s a simple formula to follow.

What are the premiums for your plan? Multiply this by 12. That is the minimum you will pay.

What is your plan’s out of pocket maximum for in-network care? Assuming your providers are in network, this is the maximum you will pay.

Add these numbers together. This is likely the high end of what you would pay. Compare the options you have on the marketplace or through your employer.

For a single person, a PPO plan might have premiums of $450 / month, a deductible of $5,000, and an in-network out-of-pocket maximum of $10,000. That is $5,400 / year in guaranteed costs and the potential for another $10,000 in in-network costs. Remember your premiums do not count against your out-of-pocket maximum or your deductible.

You might compare this plan to a HDHP with premiums of $330 / month, a $7,000 deductible, and an in-network out-of-pocket maximum of $12,000. This is $3,960 in guaranteed costs, and a potential for another $12,000 in out-of-pocket costs.

In this example, your guaranteed costs are ~$1,500 / year lower with a HDHP, but your deductible increases $2,000. To decide if the HDHP is right, look at the procedures you have coming up this year and your ability to pay out of pocket.

If the premiums for a high-deductible plan are much lower than those for other health insurance options AND the out-of-pocket maximum is comparable or not much changed, a HDHP with an HSA is likely worth it.

Note: if you will have out of network care, consider your out-of-pocket maximum for out of network care. Sometimes this can be unlimited. Consider how feasible it is to stay in network given your family’s healthcare needs.

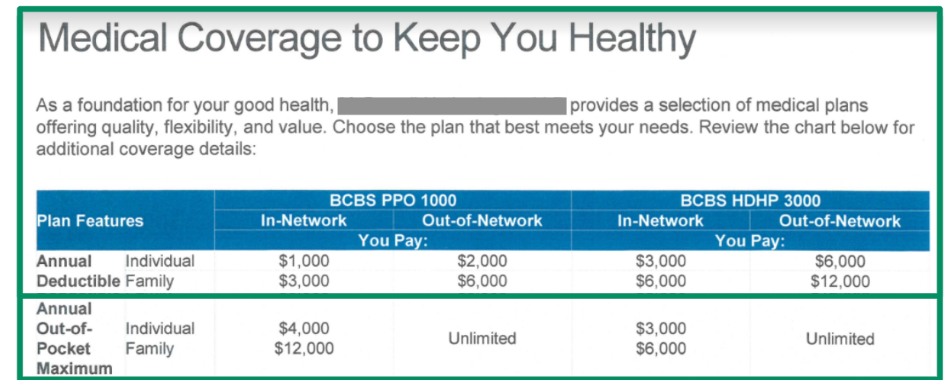

While planning for pregnancy which health plan is better PPO or HSA eligible HDHP?

Pregnancy can come with a lot of known and unknown costs. One of the best ways to pick insurance is looking at your plan’s out-of-pocket maximum. If your out-of-pocket maximum is comparable between an HSA-eligible, high-deductible healthcare plan (HDHP) and a PPO plan that is not HSA eligible, using an HSA could be beneficial. This allows you to save on taxes while paying for prenatal, delivery, and postnatal care.

Often, a HDHP is likely NOT the best option during pregnancy since you may pay significantly more out of pocket. Read the details of your plan during open enrollment to decide.

Some plans have specific pregnancy coverage. Other plans do not. In the below example, the deductible is much higher for the HDHP, but the out of pocket max is actually lower making it a good option during pregnancy. Read the fine print to make a decision that is right for you.

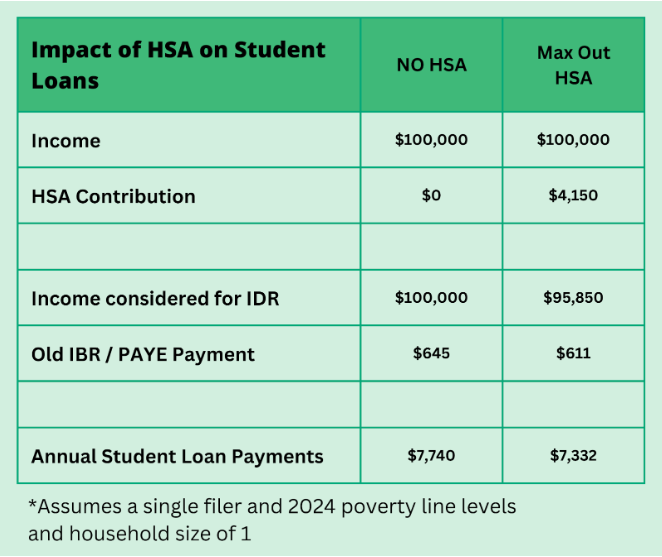

Using an HSA to lower student loans

While an HSA can not directly be used to pay off student loans it can be a valuable financial resource to make loan repayment easier. Here’s how:

- Contributing to an HSA saves you on taxes by lowering your Adjusted Gross Income (AGI)

- If you are using an Income Driven Repayment plan like SAVE, lower AGI translates to lower loan payments

Conclusion

Whether an HSA is worth it really depends on how much you go to the doctor and if you can afford to pay out of pocket for some costs. HSAs are a great way to save for retirement and lower your taxes. If you are a high earner in a higher tax bracket, a healthier individual, or if you are on an income-driven repayment plan for student loans, consider an HSA.

A big perk of HSAs is they are NOT use it or lose it. As a result, they can help you save for future medical expenses, in or before retirement. They can also be used as an extra source of funds during your golden years. The HSA is the most tax preferred account out there, and is a great way to build wealth. You should consider maxing this out before you even contribute to an IRA.

About the Author

Eryn Schultz is a financial educator and CERTIFIED FINANCIAL PLANNER® and the founder of Her Personal Finance. Eryn provides financial education events on investing, prioritizing financial goals, student loans, etc. Her mission is to help high-earning women take charge of their financial future and she has helped hundreds of women pay off student loans, save up for a down payment, diversify out of RSUs, and finally feel comfortable investing in and outside of a 401K. You can see more of her content here on LinkedIn and IG.

Uncover your money story and establish your financial baseline with this free resource that will help you chart your current money path and help you discover where your money currently flows.