A version of the same question keeps coming up from so many of you.

It boils down to this: Do I prioritize a low interest rate or do I prioritize my life?

Here are two examples that perfectly capture the dilemma many of you are facing:

- “You’re sitting on a too small, can’t renovate home @ 3% rate from ‘21. What rate would you move for?”

- “Should I keep waiting for rates to drop before I buy?”

To tackle this, I wanted to run the numbers on what a higher interest rate ACTUALLY means for your bottom line, and show you a simple tactic that can outperform a half-point rate drop.

The Mortgage Math: 6% vs. 5.5%

For the sake of argument, I assumed you are buying a **$1M house with 20% down** ($800K mortgage) using a 30-year fixed mortgage. I compared three scenarios:

- Scenario A: 6.0% interest rate, no extra payments.

- Scenario B: 6.0% interest rate, one extra payment* annually.

- Scenario C: 5.5% interest rate, no extra payments.

*In this example, one extra payment equals $4,796.40 per year.

| Scenario | Monthly P&I Payment | Total Interest Paid | Payoff Term |

|---|---|---|---|

| A (6.0%) | $4,796.40 | $926,704 | 30 years |

| B (6.0% + 1 extra annual payment) | $4,796.40 | $730,286 | 24.6 years |

| C (5.5%) | $4,542.49 | $666,295 | 30 years |

A 0.5% drop in interest rate (Scenario C vs A) is worth approximately $260.4K in interest savings and significantly lowers your monthly payment.

The Game-Changing Tactic

Here’s the powerful insight: You can drastically reduce your interest paid by committing to an extra principal payment on your mortgage each year.

Making just one extra annual payment (Scenario B vs A) has the impact of shaving $196.4K off your interest paid AND it reduces the time to pay off your mortgage by 5.4 years.

In fact, the numbers show that making two extra annual payments on a 6% mortgage can result in greater interest savings than securing a 5.5% rate.

While not everyone can afford the extra principal, this is a great option to consider if you have a bonus or other variable income. The key is understanding you have control over the lifetime cost of the loan, regardless of the Fed.

The Bottom Line: Four Questions Before You Wait

The analysis shows that financial tools minimize the impact of a higher rate. When considering the current market, here are the four key questions I recommend you ask yourself:

1. When Will Rates Drop?

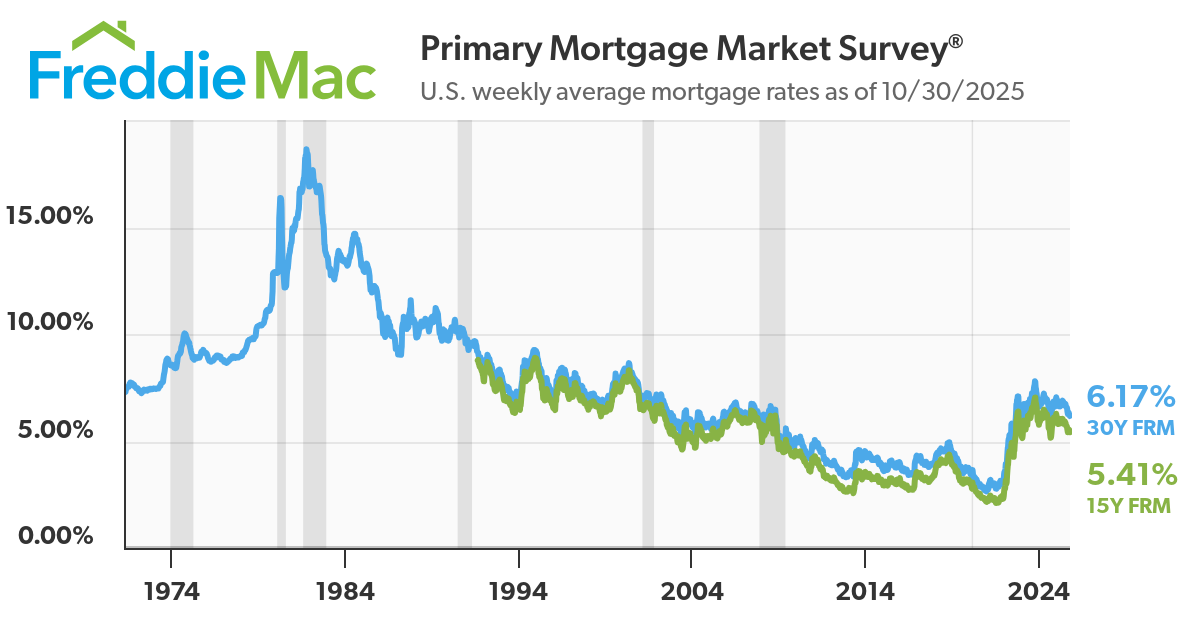

Historically, interest rates have moved slowly. While the Federal Reserve has penciled in potential rate cuts for December, inflation remains sticky. Waiting 6 months to 1-year to buy is unlikely to see more than an 0.5%–1.0% change in rates. The reality is, we do not know how rates will move. See table below for how they have moved over time.

2. What is the Cost to Your Quality of Life? (The Emotional Toll)

Are you content where you are, or are you truly bursting at the seams? If your current space is negatively impacting your well-being, moving may be the right decision. Money is a tool, not an end in itself.

3. Can You Truly Afford the Higher Payment? (The Financial Reality Check)

One major downside of higher rates is higher monthly payments. Before you make a move, confirm that you can keep your total housing costs below 28%, and ideally 22–24%, of your pre-tax income.

4. My Personal Decision

For context, my family and I are currently under contract on a new home. Running the numbers, moving is probably a wash financially and will increase our monthly housing costs by 38%. This decision is supported by academic research that highlights that renting is often the better financial decision, even if renters tend to have lower net worth. For us, non -tangible elements of owning, e.g., stability and a nicer space, beat out over the lower costs and flexibility of moving. We are ready to plant roots and lean into stability.

If you want to go deeper into your own personal situation, please reach out at eryn@herpersonalfinance.com. I would love to help you achieve your financial goals. You can read more about my firm and the work we are doing to offer hourly, fiduciary advice to more women and couples with MDs, MBAs, and JDs here.

Uncover your money story and establish your financial baseline with this free resource that will help you chart your current money path and help you discover where your money currently flows.