A recent Instagram post proclaimed that having a third kid is the new Birkin bag. As a CFP® and a mom to two young boys, that post got me thinking the necessary salary to comfortably afford a third kid in a high cost of living area like Boston, New York or Austin.

Census data shows only 14.4% of households made more than $200,000 in 2023. Yet, my experience as a financial planner and a mom in a high cost of living area, has shown me that a salary of $200K does NOT comfortably support a family of five. How much is enough? I ran the numbers and landed on or around $300K as the minimum to have three kids in a high-cost of living area. Read: not comfortable but minimum.

If you’re reading this and thinking, “I will never make $300K and I want a big family,” there is a path! These numbers assume saving for college, annual vacations, and living in high-cost of living areas. You can cut some of these things out or grow your income.

Alternatively, you may say, “I earn $300K and it still does not feel like enough.” That’s also ok. You may have some room in the budget to cut. If you are unwilling to make certain sacrifices, you can stick with a smaller family or find a way to grow your income.

Let’s run the numbers

High earning families spend $26K+ year per child

The USDA compiles a regular report on what Americans spend to have a kid. The report found that in 2025 dollars, higher-income Americans (those earning $144,336 or more in today’s dollars) spend ~$26.6K / year per child.

These costs include allocation of costs for food, transportation, housing, and childcare which are difficult to isolate.

To simplify the analysis and to avoid double counting key numbers like housing and transportation, I created my own build up of childcare costs. I used the Department of Labor average for childcare costs in large population areas. This is $16,550 per child in 2025 dollars. I then made assumptions about additional costs for groceries, transportation, and discretionary spending. I will get into those detailed assumptions below.

So, what would you need to earn to be able to pay for these costs?

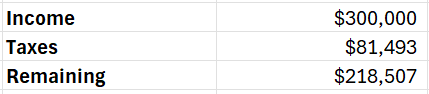

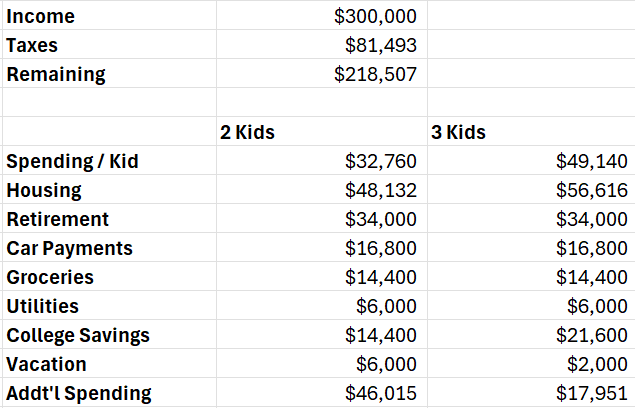

I looked at a scenario where a couple, let’s call them Leslie and Miguel, are earning $300K in household income. They live in Massachusetts and pay state income tax there of 5%. This translates to $81,492 in Federal and State taxes.* They have three kids.

I used my financial planning software, RightCapital, to do a mock build up.

If Leslie and Miguel earn $300K and pay $81.5K in taxes (this includes a 10% allocation to pre-tax 401Ks), that leaves them with $218,507.

Leslie and Miguel’s $219K in net pay is a high number. However, it is quickly eaten up paying for children, housing costs, retirement contributions, car payments, groceries, and utilities. It also tells a story of the housing crisis in the U.S.

Childcare Costs

First off, having three kids instead of two, increases their childcare and education costs from $33K to almost $49K. That’s a difference of $16K assuming $1,365 / month in monthly costs. Notably, this aligns with childcare costs I have seen from some past clients. However, it is less than what many clients in particularly expensive places like Boston and San Francisco spend on a monthly basis.

Your costs may differ depending on the age of your kids. However, it’s important to note that childcare costs do not go away as kids get older. In fact, the USDA data shows that while dips when children turn six, it jumps back up in late high school.

Outside of childcare, having more kids also means you likely need a bigger house.

Housing Costs

To go deeper into housing, this is the biggest expense for most families, including Leslie and Miguel.

The average size of a 3-bedroom house in the US is 1,700 – 1,800 square feet. If you want a fourth bedroom, a nice to have if you are going to have a third kid, that size increases to ~2,000 square feet. Price per square foot varies widely, but since many of my clients live in high cost of living areas, I used $550 / square foot. At $550, a 1,700 square foot homes costs $935,000. A 2,000 square foot house costs $1.1M.

I assumed Leslie and Miguel bought a house prior to 2022, before housing prices and interest rates jumped. This example uses a $1.1M house (2,000 square feet at $550 / square foot) and a 3% interest rate with 20% down and 0.8% property taxes. Affording a 2,000 sq ft house is a big reason having a third kid would make Leslie and Miguel feel squeezed.

Furthermore, this model would allow Leslie and Miguel to rent spending $4.7K / month. However, it does not allow for buying similarly priced homes at current interest rates. Going from a 3% to a 6.37% mortgage rate would increase the cost of a $1.1M house (only 2K feet in an area with $550 / month in cost) over $21K per year.

(Note: This analysis does not factor in any changes to your tax bill from owning versus renting. The new One Big Beautiful Bill does include tax incentives for home owners.)

Discretionary Spending

At $300K in income, Leslie and Miguel have ample room for spending on discretionary items when they have two kids. When they have three, their discretionary spending ability drops. This bucket includes “fun” and also some lumpy but necessary spending e.g., car repairs, medical bills or veterinary costs, and teacher gifts. It also includes concert tickets, eating out, holiday gifts, spending money on clothes and shoes.

If Leslie and Miguel decide to have a 3rd kid, they would need to cut ~$28K in annual discretionary spending and reduce their vacations. In this scenario, their discretionary spending drops to $15K for the year or $1.3K / month That is a tight budget and likely means they would have to cut back on college savings or make some other tradeoffs. You can always drive older cars, move further out or find a path to earning more.

Retirement and Saving for College

You might look at these numbers and say, “well, on top of not saving for college, I could just cut out the retirement savings to make the math work.” Yes, you could, but that would be a mistake. There are scholarships to pay for college. You cannot get a scholarship for your retirement. Social security will only go so far especially if you’re a high earner.

Plus, one of the biggest gifts you can give your children is your financial security. While you might need to reduce your savings rate, postpone saving for college or switch from Roth to pre-tax in your children’s early years (that will put more money in your pocket), do not stop saving for your own retirement. Modeling good financial behavior for your children is priceless.

The exception is if you already in a really good place for retirement or have a substantial inheritance that you have received or you know is coming.

Two vs Three Kids: More than Numbers

Deciding whether to have two or three kids is, of course, about so much more than numbers. As a mom of two young boys, I know firsthand the joy and chaos of a growing family. But as the numbers show, this decision also has clear financial implications that require proactive planning and an honest look at the trade-offs. Are you comfortable driving older cars so you can save for college? What about shifting to or staying in a high pay, high stress job to make the financial math work?

Coming back to the original premise of this article, having a third kid has become a sort of status symbol. Traditional luxury status symbols like a Birkin bag can be staggeringly more affordable than childcare and the other costs associated with another child. Multiple industry publications show that Birkins start at a mere $11,000. That is less than one year of childcare for a third child most places in any high cost of living area in the U.S.

For me, the decision to stick with two kids is a mixture of personal and financial. We enjoy travel, and do not want to cut back on our annual extended vacations. We value living in walkable, bikeable communities where the price per square foot is high. Plus, I experienced multiple miscarriages before my first pregnancy. The emotional and financial costs make me wary to pursue a third kid. I love our family of four, and want to focus on growing my business while my kids get bigger, and I can still run with them in a double stroller.

That’s what is right for me and my family. That may not be right for you.

Stay in touch or Work with me

This is exactly the kind of planning I do for families like yours. If you’re weighing the financial trade-offs of growing your family, stay in touch. You can sign up to get more posts like this straight to your inbox or email me to learn more about working with me one on one (eryn@herpersonalfinance.com). I love helping high-achieving women—especially those with JDs, MDs or MBAs—take charge of their financial futures and grow the family of your dreams.

Uncover your money story and establish your financial baseline with this free resource that will help you chart your current money path and help you discover where your money currently flows.