Why Did I Owe Taxes This Year & Planning for 2025

For a lot of us, tax season is an annual annoyance. We get a refund or we owe, but WHY can be a black box. For my clients, it can be particularly confusing when there are swings in the tax bill. One year, they owe a big tax bill and the next year they get a big refund. What’s happening? This article includes four numbers to check so you can understand your tax return and includes a few tips and tricks so you don’t get surprised by a big tax bill and are strategic with when and how you pay taxes.

While this article includes examples specific to women in medicine and women in tech, it is relevant to anyone trying to understand their taxes.

What should you check.

A tax return is the form you file with the IRS (or your state, if applicable) to report your income, deductions, credits, and other financial information.

While there are a lot of numbers on your tax return, there are four things that I recommend you check as a starting point: your Adjusted Gross Income; your effective tax rate; whether you owed tax or got a refund; and if you took the standard deduction or itemized. These will give you a high-level overview of how much you paid in tax, what your income is, and how you paid taxes. This can help you prepare for future years and avoid getting surprised by a big tax bill or a big refund and taking actions to strategically reduce taxes.

-

Your Total Income & Your Adjusted Gross Income

Adjusted Gross Income (AGI) is your total (gross) income from all sources (think your W2 income, interest paid from your high-yield savings accounts, some dividends, etc,) minus certain adjustments like pre-tax 401K or 403b contributions and Health Savings Accounts (HSAs). Know your AGI. Not only is this a good proxy for your income, but it’s also the number used as the cut off for some tax deductions like the child and dependent-care tax credit.

As an example, let’s say Serena and Andrew both work full-time. Serena is a physician at a non-profit hospital and Andrew works in biotech. Serena makes $250K in her role, and Andrew makes $150K including a small bonus. They have $3,000 in interest income from their high-yield savings account. Serena maxes out her 403b with $23,000 in contributions. Andrew contributes another $23,000 to his 401K. They do not contribute to an HSA or have any other income or deductions. While they have a household gross income of $403K, their AGI would be $357,000. AGI does not include their HSA or pre-tax 401K contributions. Note: Roth 401K contributions would be included.

Where can you find both numbers? Most tax returns submitted by a tax preparer OR submitting through tax preparation services like TurboTax include a summary page with this information. You can also find this on the first page of your actual return in row 11.

Tips & Tricks:

- Consider pre-tax contributions if you’re working towards Public Service Loan Forgiveness. Loan payments on income-driven repayment plans are based on AGI. This is a reason to maximize pre-tax accounts before you make Roth contributions. Roth contributions do NOT reduce your AGI. Similarly, if you are pursuing loan forgiveness and are a married couple, you may want to consider filing taxes separately.

- Check your 2024 contributions to your 401K, 403b, 457b, and HSA. In 2024, the contribution limits were $23,000 to a 401K or 403b for those under 50. HSA contribution limits were $4,150 for individuals and $8,300 for families in 2024. In both cases, maximizing your contributions will lower your tax bill today while helping you build wealth. HSA contributions do NOT have to be spent each year (read more here). HSAs can be an extra retirement account (after 65 they can be used for more than just healthcare costs) so they’re a great place to save since the money in that account is NEVER taxed. Some hospital employees also have access to 457bs which are another option for pre-tax retirement contributions.

- Don’t sleep on IRA contributions. Kunal Verma, founder of tax company Centurion Tax & Accounting shared, “A common misconception is that you can’t contribute to both [an IRA and a 401K] in the same year—you can. IRA contributions for 2024 can be made up until April 15, 2025 or whenever you file taxes.” Most individuals in medicine and tech make too much to qualify for a deductible IRA, but a backdoor Roth IRA may be an option.

-

Your Effective & Marginal Tax Rates

What was your tax rate overall? What was your Federal rate versus your state rate? The higher your tax rate, the more time you want to spend thinking about tax planning. If your tax rate is 30%, you should think about taxes differently than if it’s 15%. You can also think about how your tax rate might change in the future. If you live in New York City, but you plan to move to the suburbs next year, your tax rate will likely DROP next year. If this is you, you may want to consider maximizing pre-tax accounts, including your 401K, HSA, a dependent care FSA, etc. before you move. On the flip side, if you’re a medical trainee on your last year of your fellowship, you may want to consider Roth contributions. Your income will likely go up significantly in the future.

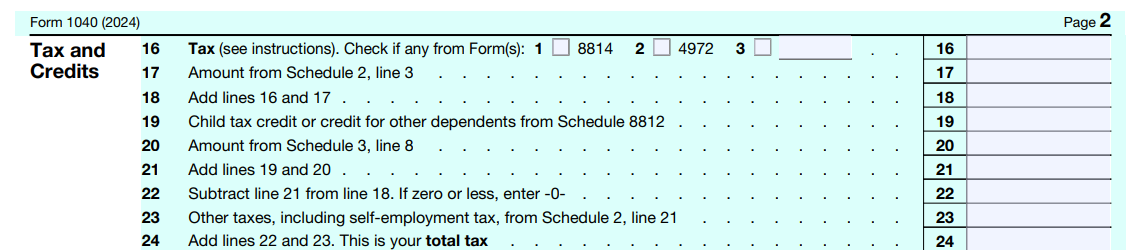

Many tax preparers and some software will calculate your effective tax rate for you. If you want to manually do this, you would calculate your total tax divided by your taxable income. Total income is found on line 9 of your 1040 tax return. You would then take your total tax owed (from line 24) and divide that by your total income (from 9).

If your total tax owed was $57,320 and your total income was $278,100 that would translate to a 20.1% FEDERAL effective tax rate. If you want to see your total tax rate, check your state return and add on the taxes that you paid there.

You can also check IRS.gov to check your TOP tax bracket. This is your marginal tax bracket. If you are a single filer earning $278,100 as seen above, you would be in the 35% tax bracket. That means any additional shifts picked up or dollars earned would be taxed at 35%.

Tips & Tricks:

- If you owed a lot in taxes or got a big refund, look at why. Did your income change from year to year? I work with a lot of women and couples in early parenthood. How did parental leave impact your income? Did you pick up fewer shifts or have a smaller bonus due to time out of the office? If you have been making the same estimated tax payments each quarter, you may need to adjust for income being lower or higher year over year.

- Pay attention to where your cash is. Many high-yield accounts were paying 4%+ in 2024. $50,000 in a high-yield account would have generated $2,000 in interest. This is free money with FDIC insurance, but it is also taxed as ordinary income at your marginal tax rate. Individuals paying 30%+ in marginal taxes, may want to consider a municipal bond fund specific to your state or a Treasury money market account that generates less in taxes.

- Try to time bonuses or extra income to fall in lower-income years. For example, if you receive an inherited IRA, you may want to push most of the distributions until after your big equity stock award vests or to years where you’re planning to pick up fewer shifts and take unpaid parental leave.

- Look for tax credits: Kunal Verma, founder of tax company Centurion Tax shared, those paying 30%+ in tax should look into “Special deductions and deferrals [that] exist for investments in historic redevelopment and opportunity zones. There are also significant credits for clean energy investments, such as residential solar upgrades, energy-rated appliances, or windows. The $7,500 federal rebate for qualifying U.S.-made electric vehicles is still available in 2025. Up to $4,000 is available for used electronic vehicles.”

-

Did you owe taxes or did you get a refund?

If you owe a small amount of taxes or get a small refund, that means you are doing your taxes right. For my clients, I define “small” as a refund or tax bill of $3,000 or less.

While people get excited about getting a refund, it means you OVERPAID taxes during the year and were giving the government an interest free loan. If you owe a large bill, you may also owe the government fees for underpayment. The interest rate on underpayment is 7% as of March 25, 2025. That’s high.

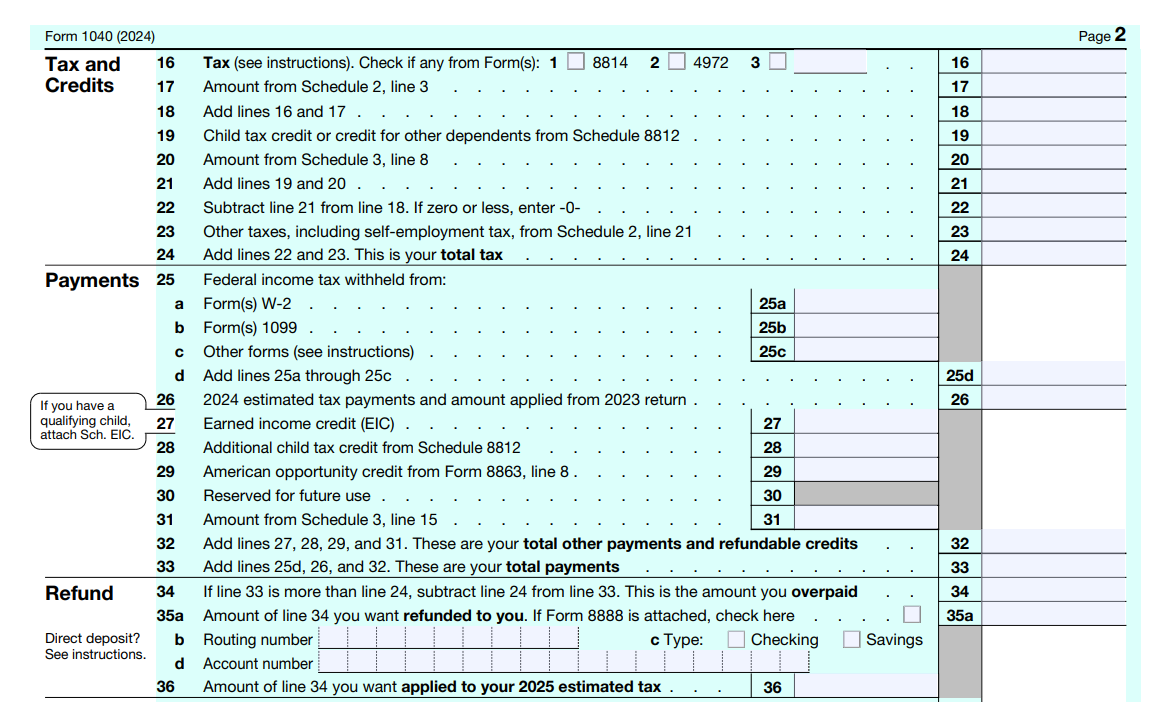

You can see if you have a refund or overpayment on line 34 (if a refund) or line 37 (if you owed) of your tax return. You can also tell from your return how much your employee withheld from your paycheck. If you had additional income, e.g., from moonlighting or from selling a large amount of company stock, you may have also needed to make estimated tax payments.

If you owe money, was it because you did not pay enough in withholdings or pay enough in estimated quarterly tax?

Going back to your tax return, look at Payments section. How does what you paid in line 33 compare to what you owed (line 24)? Did only pay tax through withholdings (box 25a) or did you also pay estimated tax payments (line 26)? Based on what you see here, you may need to change your withholdings or what you’re paying in estimated quarterly tax payments.

Tips & Tricks:

Here are a few things to consider if you owe a large tax bill OR have a large refund:

- Consider paying estimated quarterly taxes. Kunal Verma of Centurion Tax and Accounting recommends that you use the IRS withholding estimator mid-year, especially if your income varies. If you owed over $1,000 this year, consider making estimated payments. To avoid penalties, pay 90% of this year’s tax bill or 100% of last year’s (110% if AGI is over $150K). Consider bonuses, extra grants, moonlighting shifts, and stock awards (including RSUs) when mapping our your estimates.

- Pay attention to annual changes in income. Will your bonus be higher or lower? Did you or will you pick up fewer moonlighting shifts? Unfortunately, the more variable your income, the less you can put your taxes on autopilot. Your job will withhold taxes from bonuses and RSUs. However, most companies withhold all bonuses and stock awards at a flat 22%. If you are in the 32% tax bracket, your bonus and RSUs will NOT have enough tax withheld. You can adjust your withholdings or pay estimated quarterly taxes to pay the additional tax bill.

- Account for kids when making tax payments. The child tax credit can reduce your taxes by $2,000. Similarly, some childcare expenses can be deducted from your income. If you are having a baby, know your tax bill will likely be lower in the following year. These credits and deductions phase out above certain income levels so if you earn more than $400K, having a baby may not change your taxes.

- Consider pre-tax contributions. Pre-tax contributions can reduce your tax bill since they reduce your taxable income. If you are contributing Roth right now, that will lead to higher taxes today.

- Consider tax-loss harvesting. If you are investing outside of your retirement accounts, you may be able to tax-loss harvest. This is a strategy where you sell investments that are down to “harvest” the losses. That’s because you can deduct up to $3,000 in per year in capital gains losses from your ordinary income. This strategy works best when you are investing regularly in a taxable brokerage account and are in a high-tax bracket (32%+). One silver lining to the market being down is it creates opportunities to harvest some losses. Be careful with this strategy. There are pitfalls to avoid like the wash-sale rule.

4. Did you itemize or take the standard deduction?

The government gives everybody a “freebie” on their taxes. This is called the standard deduction. In 2024, if you were married filing jointly, you could subtract $29,200 from your taxes. If you were single, this number was $14,600. If you were over 65 and blind, this number was even higher.

The government also gives individuals the option to itemize deductions for things like mortgage interest, state & local income and property taxes, charitable giving, and healthcare costs. Today, an estimated 90% of people take the standard deduction. Most people spend less on the above categories than the “freebie” from the government.

If you are in the vast majority who take the standard deduction then you CANNOT deduct your charitable contributions, your healthcare costs or your mortgage interest from your taxes.

Tips & Tricks:

- If you plan to buy a house, you may start to itemize your deductions if you do not do so now. That’s because you can deduct the interest you pay on a mortgage up to loans of $750K. You can also deduct property taxes up to $10,000. This could save you money on your taxes.

- If you do NOT itemize and have philanthropic goals or plan to donate regularly, decide if you want to set up a Donor Advised Fund and make a large number of charitable donations in ONE year (a strategy called bunching) so you can itemize your deductions.

Conclusion

Understanding your tax return is key to managing your finances. Being proactive can keep you from being surprised by a big tax bill. It can also help you plan around changes in income so you can reduce your tax bill when you or your partner are finishing training or working on Public Service Loan Forgiveness. Working with a Certified Financial Planner and a Certified Public Accountant (CPA) can help you make a plan for taxes and avoid getting hit with a surprise bill. Please reach out if you want to be strategic thinking about taxes in the future.

Authors

This blog post was written by Eryn Schultz, founder of Her Personal Finance with input from Kunal Verma founder of Centurion Tax & Accounting. Her Personal Finance is an advisory firm that focuses on serving women in medicine and women in tech. Eryn is a Certified Financial Planner® professional, fiduciary, Harvard MBA, and mom to two young boys. She has a passion for helping other women and couples take charge of their financial future. She has a particular focus in supporting others while they grow their families and navigate the challenges of early parenthood.

Centurion is a professional, CPA-owned firm based in Charlotte, North Carolina, offering a broad range of services for individuals, small businesses, and their owners. Their tax offerings expand far beyond filing annual returns, based on the belief that tax savings a realized in planning and review sessions throughout the year. Centurion provides comprehensive finance and account services to a broad variety of businesses as well.

Uncover your money story and establish your financial baseline with this free resource that will help you chart your current money path and help you discover where your money currently flows.